Problem Statement: When a company embarks on an inorganic growth strategy, the question arises how to develop a playbook or methodology that makes M&A integration a most successful and repeatable undertaking. This article attempts to provide approaches and best practices to address this question, with a focus on how to scale and improve the playbook. We will not get into details of various methodologies, but rather highlight how to improve it from one integration to the next.

Scope and Time Frame Covered By Playbook

The playbook needs to cover the entire acquirer organization and is typically split by workstreams. Workstreams could be functions like HR, IT, Finance plus one or more business units that are affected by the acquisition. The overarching governance body is the Integration Management Office (IMO), which organizes and manages the integration project. Besides playbooks for each workstream, there also should be a playbook for the IMO.

The timeframe that a playbook should cover starts with the due diligence of an acquisition target and extends to the end of the integration, including capturing final lessons learned, which will benefit future integrations. During the operational diligence phase, the acquirer's integration lead needs to be involved to gain facts and understanding that drives the integration strategy. Furthermore, it is best practice to start the integration planning activities no later than 60 days prior to transaction close.

Guidance on end points of the integration should be in each playbook: When is the time reached to hand over remaining tasks to "business as usual" (i.e. the functions/BUs that own them)? What is the process for this handover and how is completion of remaining tasks tracked?

Playbooks also should cover common risks the organization faces (e.g. regulatory compliance) and how to deal with these risks. It is good practice to include risk mitigation approaches, for example a compliance or cyber security audit.

Playbook Evolution

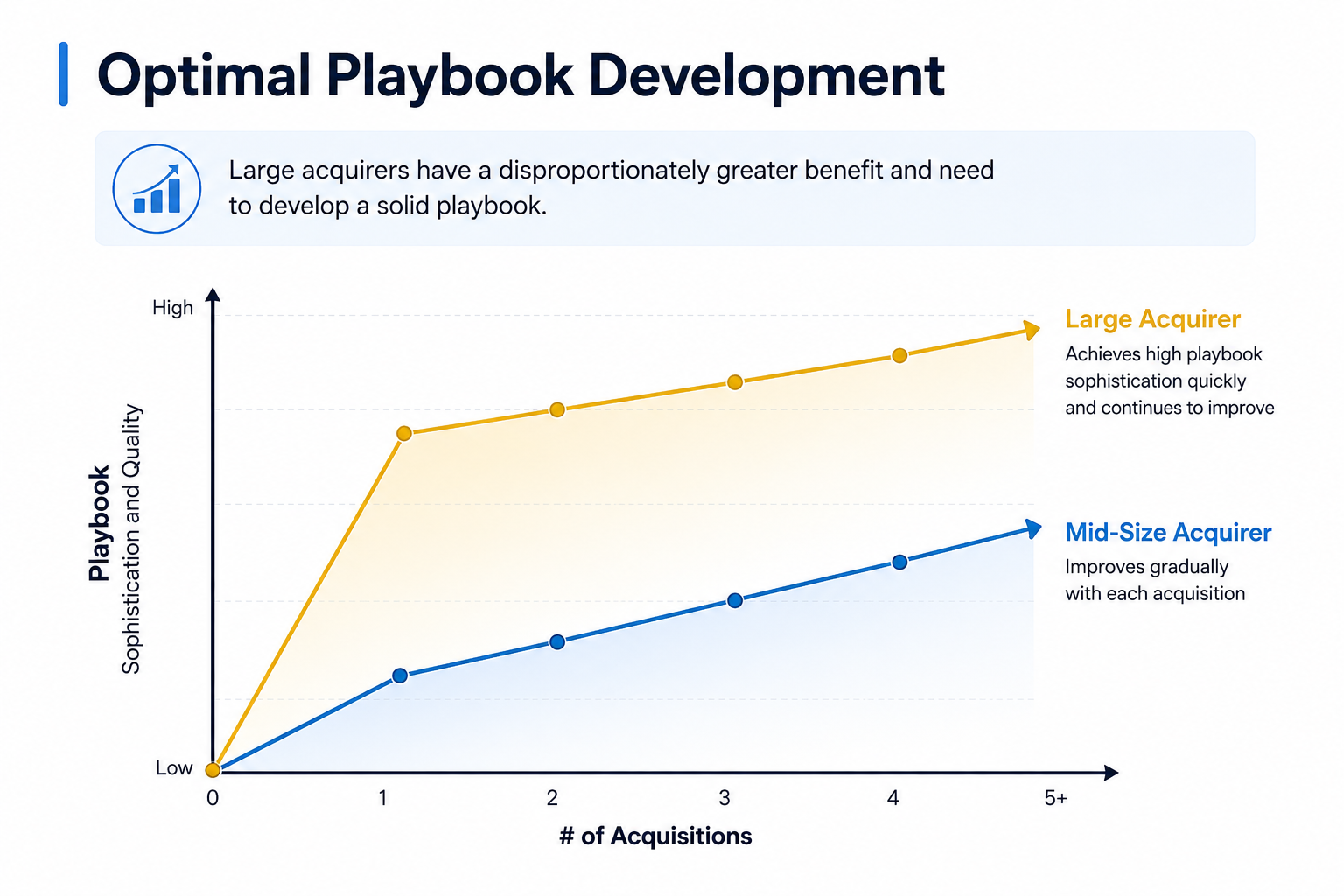

Playbook evolution depends on the size of acquirer and target: The larger the acquirer, the more detailed the playbook should be because their processes and procedures are more complex than for smaller companies. For the purpose of this article, we define two acquirer types as shown in the table below. The development of an integration will be discussed for these two types of organizations.

| Acquirer Type | Size (# of employees) | # of Business Units | Level of Documentation |

|---|---|---|---|

| Mid-Size Acquirer | < 1,000 | 1 to 3 | Low |

| Large Acquirer | 1,000+ | 4 and up | High |

For large companies, the benefits of a playbook are great from the very beginning, no matter what the size of the acquisition. This is because their organization is complex with many internal processes and procedures into which an acquiree is going to be integrated. In these larger organizations, there is very little tolerance to "wing it" — that is, to not properly integrate and fix issues as they come up. This is more costly and more time consuming (not to mention a source of executive headaches) than doing a proper integration.

For a mid-size acquirer, the sophistication of processes is lower and processes as well as personnel are more flexible. If a mid-size firm embarks on an inorganic growth strategy with many acquisitions, this acquirer understands that its processes and procedures need to mature with its growing size. While this happens, the playbook needs to reflect this increasing operational complexity. As the overall organization grows, the playbook becomes more detailed, ensuring the smooth integration of future acquisitions.

The optimal path: large acquirers have a disproportionately greater benefit and need to develop a solid playbook early. For mid-size acquirers, playbook sophistication and quality grows incrementally with each acquisition.

Challenges in Integration Playbook Development

| Challenge | How to Address |

|---|---|

| How quickly to move up the sophistication and quality curve | First and foremost, this should be driven by the need to attain synergies as quickly as possible. There are significant differences depending on cost or revenue synergies dominating the deal thesis. See more details in the paragraphs below. |

| Level of Detail | At the workstream level, the focus should be on activities that affect other workstreams. For example, revenue synergies may require a collaborative effort of a BU, Sales, Marketing, and Operations. All these workstreams should describe what their role is in planning for and attaining revenue synergies. In addition, the greater the impact on achieving synergies, the greater the level of detail should be. |

| Lessons Learned not captured | This may happen for various reasons, including lack of time and job self-preservation. The IMO needs to drive the process to capture lessons learned and ensure they get integrated into the playbooks as appropriate. |

| SMEs not contributing | Some subject matter experts (SMEs) may be so busy with regular and/or M&A integration work that they lack time to contribute to the playbook. In that case the IMO needs to step in. Perhaps more guidance is required and setting up periodic meetings to discuss progress may help. |

Playbook Focus Areas by Synergy Type

Typically there are two broad synergy categories to consider: cost synergies and revenue synergies. Whatever major synergies are expected to re-occur from acquisition to acquisition should be covered in the playbooks in great detail and early on in an acquisition program — because these synergies justified the acquisition in the first place.

For more on capturing revenue synergies specifically, see our article Revenue Synergies: Why Are They So Elusive and What to Do About It.

Cost Synergies

Cost synergies result from lowering costs in various functions of the combined enterprise — e.g. consolidation of manufacturing or office locations, lower procurement costs, consolidation of IT infrastructure. These cost synergies should be covered in the relevant workstreams. Typically, they are confined in scope to that workstream. For example: saving expenses by combining ERP systems may be owned by the IT organization. In that case, other workstreams may be involved, but the clear driver is IT.

Revenue Synergies

Revenue synergies result from increased sales of the combined organization (e.g. from cross-selling the acquiree's products, using the acquirer's distribution channels, or integrating the acquiree's technology in acquirer's products to enhance their functionality and appeal). Such synergies need to be driven by the absorbing business unit(s), with support of functions like sales, operations, and marketing.

Conclusion

A good playbook ensures the successful integration of sequential acquisitions while rapidly realizing deal synergies. It grows in scope as the combined organization expands, organically or inorganically. The authors of this article welcome any feedback and questions on this and related topics.