Management teams on both the acquirer and acquiree sides often struggle with this question. The timing may often be dictated by the deal environment. For example, if an acquirer purchases a business in a competitive bidding environment, integration planning is unlikely to start before the acquirer has won the deal. But there are other situations in which management has more flexibility — for example if regulatory approvals need to be obtained prior to deal close. Then the question often is how much time to allocate and what should be prioritized. This article sheds some light on this topic.

In this article, "Integration" refers to all aspects of operational integration of two companies, starting with integration strategy, communications and integration planning and ending with execution of those plans.

Rules of Thumb for When to Start Integrating

- A. Integration should start well before the deal is publicly announced.

- B. For private companies closing a deal that is not publicly announced: it is best practice to start 3 months prior to transaction close.

- C. The earlier the better, but thought should be given to what will be done — to avoid burnout, frustration, and duplication of effort.

The reasoning behind these Rules of Thumb:

A. At the moment of public deal announcement the world knows about it and stakeholders will wonder what it means for them. Thus, integration strategy and communication planning should definitively start before then. More importantly, integration planning should be integral to the acquisition process from the very beginning. For example, before any offer is made, high-level integration planning should establish an order of magnitude for integration cost and also the degree of challenge and/or risk associated with anticipated market or cost synergies. Each of these influences the upper bound of what offer can be made. At the time of announcement the rationale behind the deal and the approach to integration should be clear and considered to be in the press release. As an aside, even if there is a legal or regulatory waiting period, integration planning can start in most cases.

B. Starting 3 months prior to close provides a good amount of time to define the integration strategy, organize the integration team and approach, and plan in detail for the first 90 days after the transaction close.

C. This is a general guideline that applies to all deal sizes and whether it is a public or private transaction. The risks are that detailed planning in some functions may jump ahead of a fully-baked integration strategy and overall plan. This likely results in wasted effort and rework, causing frustration in the organization.

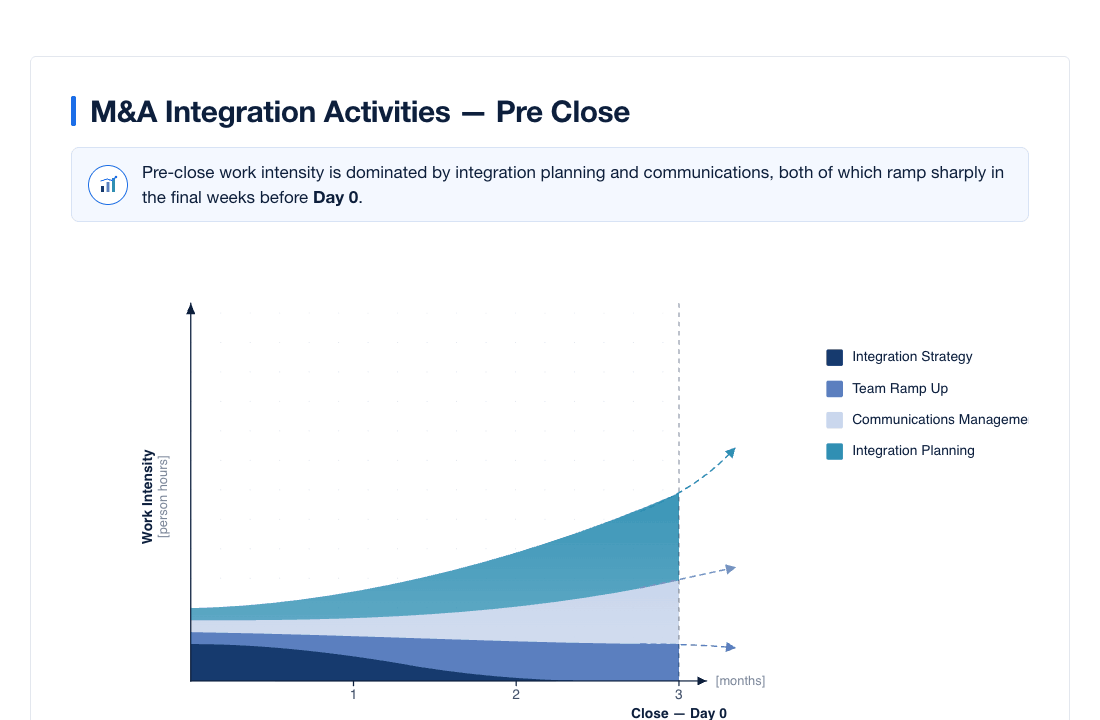

Work Intensity Before Transaction Close ("Pre-Close")

The graphic below illustrates the time commitment for M&A integration assuming start of activities three months prior to transaction close.

Integration strategy is closely tied to the perceived synergies of the deal. Discussions around integration strategy should start during deal due diligence and it should also factor into the valuation model as appropriate. Major decisions on integration strategy should be made early on, assuming that the relevant information can be obtained and key stakeholders can weigh in. Enough time should be allowed at the senior management level as these decisions often have broad business implications, need to be thoroughly analyzed and socialized with key stakeholders. Integration strategy should be completed prior to deal close.

Team ramp up starts early and typically activities around identifying and on-boarding team members continue through the deal close, but should be set within about 30 days post close, even for large, multi-billion dollar acquisitions. The on-boarding may include reviewing of applicable lessons learned from prior deals, and training on the proposed approach and methodology for integration.

Communications management gradually increases and reaches a peak within a month of close. Communications are critical from the moment the deal is announced, and Day 1/Week 1 communications planning is time consuming for every deal — and in particular for larger acquisitions that entail multiple locations in various countries. It is best practice to use a variety of communications means, and it should be noted that many stakeholders will first hear about the integration in some detail during Day 1/Week 1. Spending time and resources to ensure these activities launch without a hitch is a good investment and will set the stage for future integration successes.

Integration planning gains momentum as the development of the integration strategy progresses and key integration decisions are made. Examples of such decisions are complete or partial integration, and what are key priorities or focus areas. First deliverables relate to what is mandatory for Day 1, followed by activities that need completion by Day 30.

Case Studies

Case Study A: Cross-Border Acquisition in the Financial Services Industry

A U.S. client acquired a multi-billion dollar, publicly traded business with thousands of employees in Europe. The U.S. client was about the same size as the international acquisition. While the terms of the deal and definitive acquisition agreement were executed relatively quickly, obtaining the regulatory approvals in dozens of international jurisdictions was expected to take 8 to 10 months after deal announcement.

The client as well as the acquiree had done small M&A deals before, but nothing of this size. After establishing the key workstream leads and a governance structure, two days of M&A integration training were held to level-set all key stakeholders — including executives — on the approach, guiding principles, and objectives of the integration. This was followed by an integration kickoff for all stakeholders and subsequent kickoffs of integration planning activities in all the workstreams. This deal was considered transformative as two of the acquirer's business units were significantly impacted and changes in the business model such as go-to-market were expected. Some key elements of the integration strategy were set early, while other elements progressed slowly and had to wait until the close of the deal.

This deal was driven by revenue synergies and therefore planning for those was prioritized, with a clean room established to share sensitive information across the two companies. This sensitive information included sales by customer and customer contact data. In parallel, communications were actively managed to inform both companies about the approach and status of the integration. The intensity of efforts in the communications realm increased gradually with preparations for Day 1/Week 1 communications. After Day 1, the first phase of the communications plan was executed, while planning for future communications continued.

Case Study B: Tuck-In Acquisition in High Technology Industry

A U.S. technology client was planning to acquire a niche leader to complement its offering. The client had a similar offering, but it was not as advanced and had much less traction in the marketplace. The relationship between client and acquiree were amicable and some employees had worked at both companies over the years.

While this was a relatively small deal (less than $50M in sales and fewer than 50 employees), the client hadn't done M&A deals in seven years, so the M&A integration muscle needed strengthening in the organization. The client decided to start the integration effort two months prior to close. This allowed for properly setting up the integration governance, training of team members while planning the integration and executing on integration deliverables. In parallel, an integration playbook was developed to facilitate the on-boarding of team members in future deals and to capture lessons learned from this specific integration.